For years I have been frustrated with Zillow's Zestimates. I have countless cases where the sales prices of homes were wildly different than the Zestimates. They cause confusion and frustration every time I hear them brought up. Today was a breaking point. Even today, many years after they first started playing pin the price on the donkey, in my market they are STILL only within 10% of the sales price 53% of the time and 22% of the time, or over one in every five homes, they are off by more than 20%! … [Read more...]

Foreclosures and Short Sales Don't Matter to House Prices

July 5, 2011 by 7 Comments

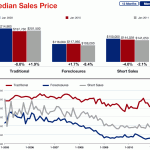

While foreclosures and short sales continue to be around 40% of our sales, when looking at housing prices I believe they should be completely ignored. When looking at all Twin Cities housing sales, here is how the Median Sales Price stacks up: When we split it out to look at Foreclosures, Short Sales and Traditional Sales, we see that Traditional Seller prices have not fallen nearly as much as the composite number suggests: Why we should ignore foreclosure and short sale sales data If we go … [Read more...]

Traditional Seller Prices Rise, Foreclosure Prices Plummet

February 12, 2011 by 1 Comment

You have Zillow, Trulia, Case/Shiller, the National Association of REALTORS and the Minneapolis Area Association of REALTORS and many others all release housing statistics that are then mentioned by local media. The beauty of today is that we have more information than we have ever had before - the problem with today is that a lot of that information is useless or misleading when talking about an individual house, a block or a neighborhood. See, housing isn't just a local thing... it is a hyper-local thing. I … [Read more...]

Minnetonka Home Sales Prices Surge Illusion

January 14, 2011 by 1 Comment

Looking at a recent copy of the Minneapolis Area Association of REALTORS' market update for Minnetonka you will see a stunning figure: Minnetonka's median home sales price is up an astounding 8% versus last year and the average sales price is still showing a healthy 5% increase over last year as well. Sounds like prices in Minnetonka are heading up right? Not so fast.... I am a huge numbers geek and while most of the time averages are a good way to understand an overall trend, in times of great flux they can … [Read more...]

Twin Cities Home Prices Fall to 5 Year Low

March 13, 2008 by 2 Comments

MAAR released figures this week that show the Median Sales Price in the 13-county Twin Cities region fell in February to $195,060... the lowest level since 2003. Sparked by strong competition and lower demand from buyers, prices have moved sharply lower in just the last few months. While this news isn't exciting for sellers, it is a very positive development for buyers in this market (and for sellers planning to buy as well). With housing affordability now at 5-year highs in the Twin Cities and mortgage rates … [Read more...]