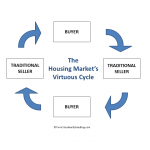

The housing market has come roaring back in many markets throughout the U.S. and some have been questioning whether the surge of activity we're seeing has staying power. In many markets, from 2008 through much of 2012 we saw that nearly half of home sales were of foreclosed or short sale properties. What we're seeing now is a return back to the Traditional Seller as foreclosure and short sale inventory declines sharply. What's crucial about this return to a more normal market is that in a Traditional Sale, … [Read more...]